Have you ever wondered how some retirees seem to sleep soundly at night, even when the stock market is having a meltdown? Chances are very high that they're using a strategy that most people have never heard of, the 3-bucket retirement framework.

Here's the thing: the title of this post promises "without market risk," but let me be completely honest with you upfront. No retirement strategy can eliminate market risk entirely. What the 3-bucket approach does is something arguably more valuable, it helps you manage that risk so effectively that market volatility becomes much less scary. Think of it as a financial shock absorber for your retirement years.

So why is this framework so powerful, and how can you use it to build serious wealth for retirement? Let's dive in.

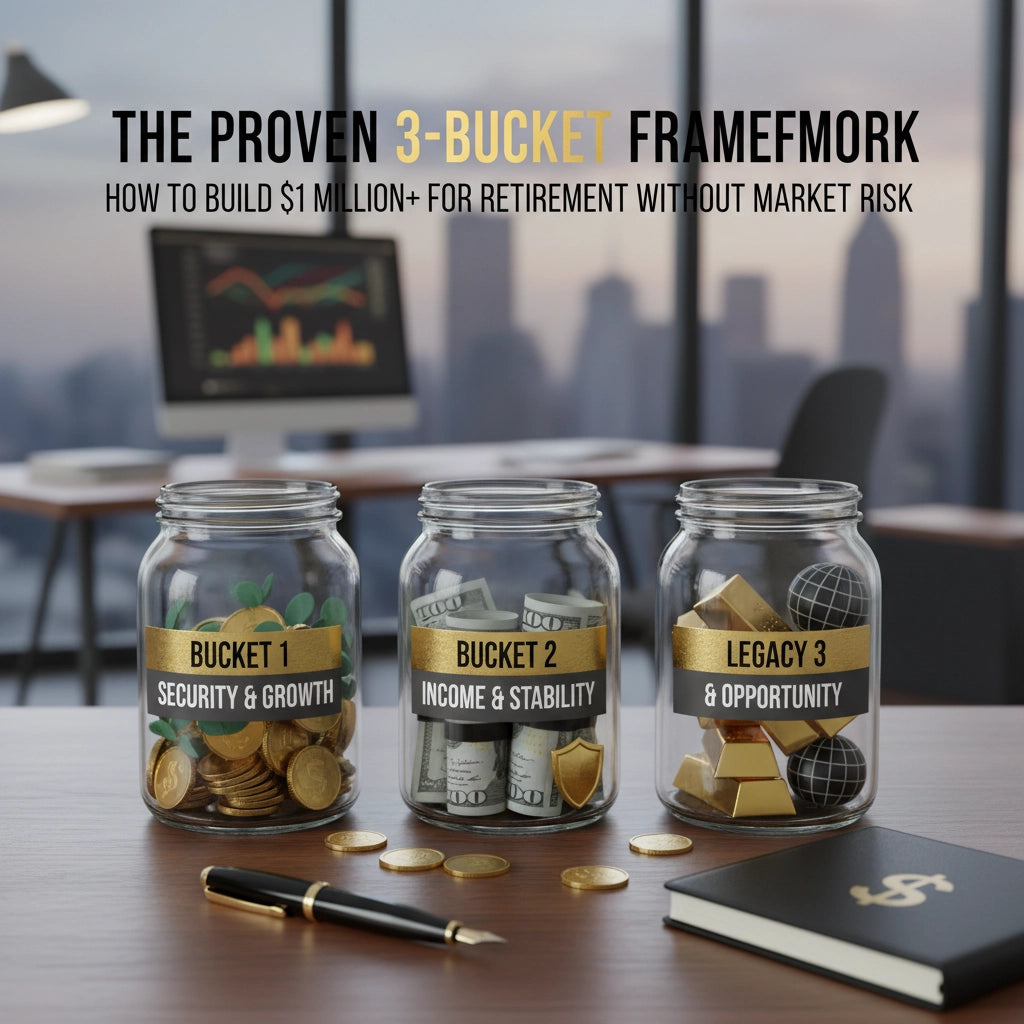

What Exactly Is the 3-Bucket Framework?

The 3-bucket strategy is beautifully simple in concept: you divide your retirement money into three separate "buckets" based on when you'll need to spend it. Each bucket has a different job to do and uses different types of investments to get that job done.

It's kind of like organizing your closet. You keep your everyday clothes easily accessible, your seasonal items in medium-term storage, and your special occasion outfits tucked away for the long haul. The 3-bucket approach does the same thing with your retirement dollars.

Bucket #1: Your Safety Net (Years 1-4) This bucket holds enough money to cover your living expenses for the next one to four years. We're talking about roughly $80,000 to $160,000 for most people, depending on how much you spend annually. This money lives in super-safe, easily accessible places like high-yield savings accounts, certificates of deposit, or treasury bills.

The whole point here is stability and immediate access. You never want to be in a position where you need grocery money but have to sell stocks that just dropped 20%.

Bucket #2: Your Bridge (Years 5-8) The second bucket covers your expenses for roughly years five through eight of retirement. This is your "Goldilocks zone", not too risky, not too conservative. Think investment-grade bonds, dividend-paying stocks, or balanced funds that can grow modestly while staying relatively steady.

If you need $40,000 per year in retirement, this bucket might hold around $240,000. It's there to bridge the gap between your immediate safety net and your long-term growth investments.

Bucket #3: Your Growth Engine (Years 9+) This is where the magic happens for building serious wealth. Bucket three holds money you won't touch for at least nine years, which gives it time to ride out market ups and downs. This bucket gets invested in growth stocks, equity funds, and other investments with higher potential returns.

Here's the beautiful part: since you won't need this money for nearly a decade, you can let it grow through multiple market cycles without losing sleep.

How This Framework Actually Protects You

You might be thinking, "This sounds nice in theory, but how does it work in the real world?" Great question. The protection comes from how you use these buckets together, not from each bucket individually.

Every year, you withdraw money from Bucket 1 to live on. Then, at the end of the year, you replenish Bucket 1 using money from Bucket 2. When markets have done well, you refill Bucket 2 using gains from Bucket 3.

But here's the crucial part: when markets tank, you simply don't touch Bucket 3. You keep living off Buckets 1 and 2 while your growth investments have time to recover.

Let me give you a concrete example. Imagine two retirees, both starting with $1.5 million. Sarah uses the 3-bucket approach, while Tom uses a traditional mixed portfolio. In year two of retirement, the stock market drops 25%.

Sarah's cash and conservative investments cover her living expenses just fine. Her growth investments are down, sure, but she doesn't need to touch them. Tom, on the other hand, has to sell stocks at a loss to pay his bills. By the time the market recovers, Tom has permanently lost a chunk of his retirement savings.

This is what financial experts call "sequence of returns risk", the danger of needing money right when markets are down. The 3-bucket framework is specifically designed to solve this problem.

Building Your Way to $1 Million and Beyond

Now, how do you actually implement this to build substantial retirement wealth? The framework works best when you're already approaching or have reached your target savings, but the principles can guide you throughout your working years too.

The Million-Dollar Allocation If you've built up $1 million in retirement savings and need about $40,000 per year to live on, here's how you might divide it:

- Bucket 1: $80,000 (2 years of expenses)

- Bucket 2: $240,000 (6 years of expenses)

- Bucket 3: $680,000 (your growth engine)

Notice that the majority of your money: about 68%: stays invested for growth. This isn't a conservative strategy that parks everything in CDs. It's a smart growth strategy that eliminates the timing risk.

During Your Building Years While you're still working and saving, focus on maxing out your tax-advantaged accounts and building toward that million-dollar goal. The beauty of thinking in buckets early is that it helps you plan more strategically.

You might keep a smaller emergency fund (your proto-Bucket 1) while investing more aggressively in your 401k and IRAs (future Buckets 2 and 3). As you get closer to retirement, you can start shifting some assets toward the more conservative buckets.

The Psychology Game-Changer

Here's something most financial articles won't tell you: the biggest benefit of the 3-bucket approach isn't mathematical: it's psychological. Market volatility becomes much less stressful when you know your immediate needs are covered.

Think about the last time the market had a rough patch. If you're like most people, you probably checked your retirement account balance, felt a little sick, and wondered if you should "do something." With the 3-bucket approach, market drops become almost irrelevant to your day-to-day peace of mind.

You know you have years of expenses covered in stable investments, so you can actually hope the market stays down longer. Why? Because it means your Bucket 3 investments are "on sale," and you'll benefit more when things turn around.

What to Watch Out For

No strategy is perfect, and the 3-bucket approach has some limitations you should understand.

It Requires Active Management You can't just set this up and forget it. You need to rebalance between buckets periodically and adjust your allocations as you age. If you're not comfortable managing investments or working with an advisor, this might not be the right approach for you.

Cash Drag During Bull Markets During strong market runs, keeping large amounts in cash and bonds will cost you some potential gains. The trade-off is worth it for most retirees, but it's something to consider.

You Still Need Substantial Savings This framework helps manage risk, but it doesn't create money out of thin air. If you haven't saved enough for retirement, no allocation strategy will fix that fundamental problem.

Getting Started With Your Buckets

Ready to implement this for yourself? Here's how to take the first steps:

- Calculate your annual retirement expenses - Be realistic about what you'll actually need to spend

- Determine your bucket sizes - Use the guidelines above as a starting point, but adjust for your situation

- Choose appropriate investments for each bucket based on their time horizons

- Set up a rebalancing schedule - maybe quarterly or annually

- Consider working with an advisor who understands this approach

The 3-bucket framework isn't magic, but it's close. It takes the emotional chaos out of retirement investing and gives you a clear, systematic approach to managing your money. More importantly, it lets you sleep at night knowing that regardless of what the market does tomorrow, you're prepared.

If you're interested in learning more about how this strategy might work for your specific situation, comprehensive planning can help you determine the right allocation for your buckets. And if you want to dive deeper into the concept, our 3 Buckets to Build Wealth service walks you through the entire implementation process.

The path to a million-dollar retirement isn't about eliminating all risk: it's about managing risk intelligently so you can build wealth while sleeping soundly. That's exactly what the 3-bucket framework delivers.